Variable Unit-Linked Life (VUL) is a financial instrument that can help solve financial problems you are or will be facing. It’s also known as Variable Universal Life. Whether we like it or not, we all have financial realities to deal with, and they are universally true.

For example, being a breadwinner gives you worries like “how will my children eat and go to school if I’m gone suddenly?” “How will I sustain my lifestyle when I retire?” “How will I cope if a critical illness sets in?” Thankfully, there’s VUL that can help.

Our Current Realities That Can Drive The Need for VUL

1. Investing is hard. Life demands us to be responsible. Obligations abound. Bills are horror films- they’re scary. 3-Day sale are always flashing. Shopping Apps are notifying. But, are most of what we purchase depreciating assets? In short, it’s difficult to invest for the future. There must be a way.

2. Financial Goals – whether we like it or not, financial needs will come. That child will reach college. College tuition fees are rising. Even if public college will cause you to raise allowances. You’ll retire, you’ll have parents who’ll need support, you’ll need a shelter. You will get sick. All these are realities we shouldn’t deny. Instead, we’d have to face courageously.

3. Travel and recharge – we get stressed. We miss our families. We need to catch up. We need to detox. You’ll face the need to have rest in the future and a well-prepared travel plan will help you enjoy the most. You need the have a S.M.A.R.T. goal.

4. Breadwinner situation – at some point, you are supporting someone. But the reality of death can come anytime. Hebrews says, “it is appointed for a man once to die…” Death is certain. Question is, “will your dreams or goals for your family die also?”

5. Debt and Emergency Funds – survey says that 9 out of 10 Filipinos have experienced shortage in the last 12 months.

6. Retirement – studies show that only 1% can retire comfortably. 76% depend on their relatives. 23% continue to work during their old age. Did you know that it takes P5M to P15M to retire comfortably in the Philippines? P4,704 is the average SSS pension and P18,945 is the highest. Most millenials and Gen. Xers now belong to the “Sandwich Generation.” Meaning, they support both their ageing parents and their children.

Realities may be hard to swallow. The “truth hurts” as the saying goes. But being wise and future-oriented is also a choice. Wisdom and prudence are god-like themes of the Book of Proverbs. Question is, where does your money go? How is your preparation? With VUL, you can help solve some, if not most of the current realities above.

About The Solution-Provider

Just a disclaimer, I’m a Licensed Insurance Advisor from under the Philippine Insurance Commission. My professional mission is to help customers achieve LIFETIME financial security.

To do this, I assist my clients in creating, implementing and reviewing their financial plan as an Insurance/Financial Advisor. I help people increase their financial awareness and develop their financial literacy.

The life insurance company where I belong started in 1865. It provides a diverse range of protection and wealth accumulation products and services to individuals and corporate customers worldwide. It has key operations in Canada, US, UK, Ireland, HongKong, Japan, China, Philippines and more. SunLife consistently ranks as the top 1 insurance company in different categories.

My video presentation on “What is a VUL” using a Pot of Gold Illustration

What is VUL? (Insurance with Investment)

Variable Unit-Linked Life (VUL) plan is an investment-linked life insurance policy that gives both protection and opportunity to grow savings over time. It’s targeting two goals with one action- to secure income and to grow money.

- Variable because client can choose or vary which instrument he or she can place his money in. Owner has the choice of investment funds. Cash value depends on investment performance.

- Unit-Linked because a your payments, after charges, are converted into “fund-units” and invested for growth. Also referred as Universal which comes from the Universal Life, seen as a savings account with flexible premiums. Interests are credited to account value.

- Life Insurance because its basic offering is to take the risk whenever something happens to the life of the insured. If the insured is taken out of the picture, VUL will carry-out the agreed responsibility to the beneficiaries of the insured.

What's in it for you? the VUL COncept

Diversification

“Don’t put all your eggs in one basket.” This is a tried-and-tested principle in investing. If we’re humble enough, we can admit that no one knows the future- even the market. All we can do is make an educated risk-taking and well-informed decision-making. VUL allows you to diversify by putting your assets in various instruments.

Professional Management

Specialization is the key to progress. The more you devote your time and energy to things that you do best, the more successful you can become. With VUL, you can devote your focus to your profession, and entrust your VUL investment to professionals who’ve been doing it for decades.

Flexibility

VUL allows you to be flexible with your payment premiums and investment activities. Compared to Traditional, trad insurance policies don’t allow flexibility. When it’s your due date, it’s time to pay the exact amount at the right time, or the policy will lapse. With VUL, you can pay more now and may skip later if you have emergencies. You can top-up premiums to boost your investment.

Access

You can usually access your policy portal anytime and anywhere using the internet. It’s also like accessing your online bank. As a client, you should be able tosee your policy details, fund value performance, contacts, beneficiaries, etc. on your online portal. You enjoy the convenience of paying through credit card, auto-credit, auto-debit, bills payment, pay thru financial apps, pay at malls, pay at remittance centers and more.

Administration

VUL charges a so called Administration Charge. It’s because you have an entity you can go to anytime. There are city offices in strategic cities or centers where you can address any concerns. You may use the facility to meet with an advisor. You can also pay there, ask for infos, get your claims, withdraw investments or dividends, and more.

Transparent Charges

At VUL, you can see the charges both in the proposal (fund projection) and your online portal. The charges are transparent and are updated regularly.

Client is Involved

VUL gets you involved as you decide where to put your investments. You can also decide what add-ons or riders to integrate to your VUL insurance policy. You may see them below.

Needs-Based Financial Planning

The best way to determine your VUL policy is through a well-planned needs-based selling system. This is a proven and effective system practiced by most satisfied clients and most successful financial planners.

Not all clients have the same financial needs. We have different goals, needs, capacity, gifts and risk appetite. There is no one-size-fits-all VUL policy for everyone. The best and most respected way to avail a VUL is to work with an advisor to determine you financial needs and investment risk appetite.

Benefits of Financial Planning

- For the Client – this system provides a long-term and holistic perspective on financial planning. It paints a vivid picture of where the client is right now and where wants to be in the future. This picture will help him choose solutions that will bridge the gap between his present financial situation and desired future state.

- For the Advisor – once a financial need or goal is clearly identified, the client sees the advisor’s recommendation as a solution that enables him to accomplish his financial goals. The advisor is viewed as a solution-provider and not a disruption or product-peddler. This leads to improved and better relationships.

- For the company – The needs-based system is the cornerstone of quality sales practice. For example, Sun Life adheres to this system to maintain the highest code of market conduct. It’s also a manifestation that the company stays true of its advocacy on financial literacy.

To fully appreciate its essence, continue reading until the end of this post. There’s a form that you can fill-up to help you assess and find a financial solution.

What are the benefits of VUL Insurance?

VUL basically helps you in two ways: Death Benefit & Fund Value. Below are the explanations.

DEATH BENEFIT

is the guaranteed amount that your beneficiaries receive the moment you move on to the next life.

This helps solve your worldly worries such as “how can my children eat when I die?” “how will my parents survive old age incase I pass away first?” “how will my spouse sustain my family + supply for my family knowing she’s a housewife?”

FUND VALUE

the amount invested to your chosen instrument for the opportunity of growth over time.

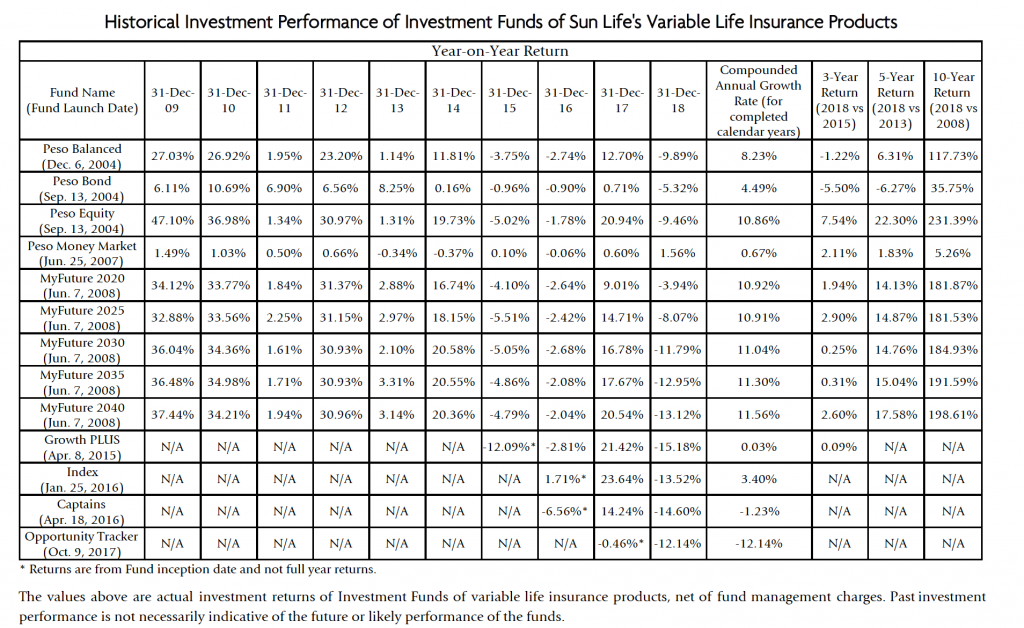

Since it’s an investment, the growth is not guaranteed. It’s good if you first determine your risk appetite and timeline before choosing where to put your money. I can help you. You can see historical performance of a certain fund instruments so you can see how low or how high it goes on certain years.

Add-Ons that Can Be Added to VUL (Riders)

Death benefit and fund value are the bread and butter of VUL. But you can enjoy to add the following riders or add-ons. These are also depending on the insurance company. But at Sun Life, these are our add-ons

Total Disability Benefit (TDB) – when added, your VUL policy fees are waived the moment you are permanently unable to work for life. You no longer have to pay your VUL policy and you’re covered for life. This incurs additional cost to your premiums.

Accidental Death Benefit (ADB) – adds a guaranteed amount incase the life insured dies by accident. Additional cost applies.

Accidental Death, Dismemberment and Disablement Benefit (ADDD) – when the life insured suffers bodily losses such as loss of foot, eyesight or fingers, the company will pay you up to 100% of the Face or guaranteed Amount. Or when the life insured is disabled due to accident, he or she receives a payout (conditions apply).

Critical Illness Benefit (CIB) – if the life insured contracts one or more of the listed Critical Illnesses or has undergone specified surgeries, he or she will receive the guaranteed amount. There are some conditions like 90 days after the policy comes into force, before the insured’s 70th birthday and other conditions.

Why is VUL a Good Investment?

VUL is sometimes being criticized. There are many “gurus” out there who say that you should “get a term insurance and invest the rest.” The problem with this mindset is underestimating the labor in doing investment research. If you have all the time, energy and knowledge to do the investment venture or stock market chart analysis, then that could be true to you. But how about your work? Your business? Your family?

I am a stock investor too and I experience it is overwhelming to juggle all those information, analysis and charts just to make an investment decision. At the end of the day, it’s better to leverage the expertise of a group that devote 100% of their time managing growth. If you have no desire or time to learn the deep technicalities of stock markets, bonds and other investments. But remember, the growth is not guaranteed and the historical performance is not a guarantee of future.

Leveraging the Expertise of Fund Managers

The best thing with VUL is that you stay insured and is using the expertise of well-educated and licensed investment fund managers. They devote their time studying companies and finding out where to put your money. VUL will save you from frustrations and big investment mistakes because you have managers doing the job. Even SSS (Government-led social insurance in the Philippines) uses privately-managed funds to invest their money in.

In VUL, your investment funds cover the the insurance charges. Looking forward to the future, you won’t even mind it because there would come a time, when your fund is big enough, that it will auto-pay your insurance charges. You may not mind them for some time but review them regularly.

Flexibility, Future-Usefulness and Advisor's Support

Unlike getting a term or traditional insurance, you pay more as you get older and you may be tempted to stop. If you miss paying, you will need to reinstate or reapply and will be under several limitations again just like as a new applicant. Worst case, when you’re already diagnosed, you may be disapproved.

If you will have rough times in the future, VUL can sustain you in three ways: (1) You can withdraw from your fund value for emergencies (2) You can rest from paying given that your fund value can pay for the insurance charges (3) The growth of your fund is used to pay your premiums in the future. Plus you can withdraw them.

VUL helps you to have invest by receiving constant reminders of your premiums. A VUL comes with a Financial Advisor whose job is to remind you of your regular contribution. It’s like hiring a financial consultant who specializes on setting aside money to help you secure income and reach your financial goals.

How Does VUL Insurance Work?

VUL Pros and Cons

Pros

- Part of premiums go to investments.

- You choose which Investment Fund to put in, depending on your risk appetite, horizon and goals.

- Policy owner is reminded to pay regularly.

- When you miss payment, fund value can cover up charges (if sufficient).

- You can add other benefits like Critical Illness, Hospitalization

- Funds are withdrawable anytime

Cons

- Returns of Investment are not guaranteed. Depending on the chosen fund and performance.

- You pay higher than the traditional policy because some go to investments and investment management.

Where are Investments Placed?

VUL allows you to choose where to place your funds. The fund placement is determined by multiple factors (See “11 Factors…” below) These factors include your investment horizon, risk appetite, life stage and more.

There are 5 major fund instruments to place your money in. Please note that at VUL, risks are solely borne by the policy owner.

[table “” not found /]

After you have built your emergency savings, better start investing. Compared to storing it your money in the bank or other very low yield instruments, it’s wiser to put them in growth funds according to your risk profile.

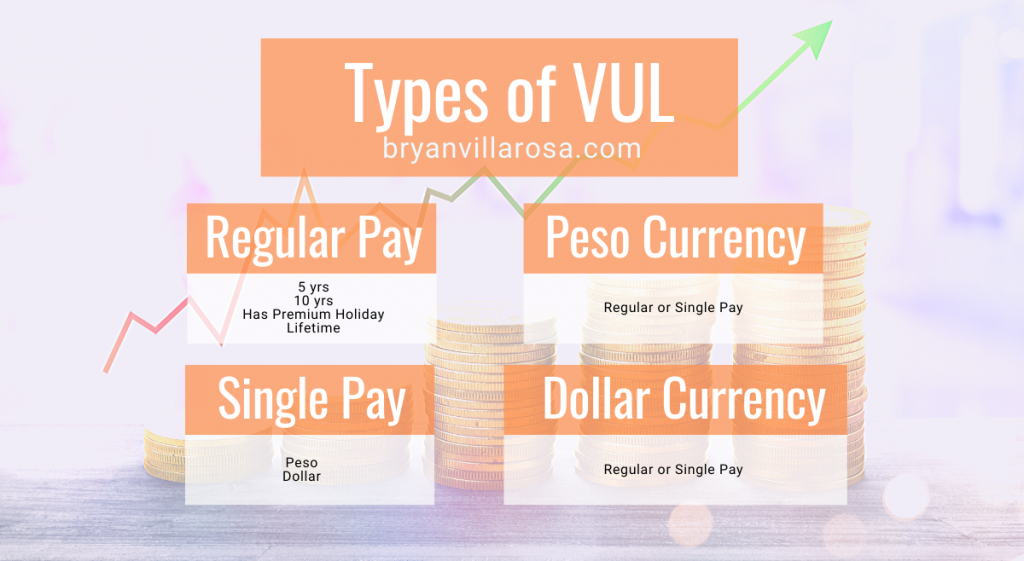

Types of VUL (Insurance + Investment)

VUL-Related Terminologies

Face Amount

The guaranteed or promised amount to the client. It’s given 100% or a percentage of it when the stated risk happens to the client. This is usually where Death Benefit is taken from.

Fund Value

The funds invested to different investment instruments. This is where insurance and periodic charges are taken from. This is the amount worked out for your future needs.

Premiums

The amount you pay to the insurance company. A portion goes to premium/admin charges, the rest goes to your fund value.

Units or NAVPS

Net asset value per share or NAVPS represents the value of your investment shares.

Premium Holiday

Refers to the cessation of premium payment under a VUL for a period of time with a view to continue later on. If a VUL is not designed to be limited-pay (paid for a period of time), premium holiday can be applied by the advisor.

Excess Premiums

The amount added on top of your policy to be added to your investment fund.

Living Benefits

The services or benefits that the client will enjoy aside from the death benefit. Living benefit usually refers to the withdrawable funds, hospital income benefit rider, critical illness rider, etc.

Riders or Add-ons

The benefits added on top of your VUL policy. This refers to health insurance, hospital reimbursement, accidental death, disability benefit, female critical illness.

SAMPLE COMPUTATION OF VUL

Eleven (11) FACTORS TO CONSIDER BEFORE GETTING A VUL INSURANCE

Below are the factors that can help determine the best VUL Insurance customizations that will suit you best.

I. Your Life Stage and Concerns

A life stage is not primarly about age. It’s about the your condition and your priorities. It is defined by your set-up and financial goals.

1. Getting Started Lifestage

You are building confidence and independence. You are lifting off from your new path. You are enjoying the freedom of working and gaining. Your career is helping you to help others.

- Day-to-Day Expenses

- Building savings to achieve personal goals

- Growing emergency funds

- Protection for yourself and your parents

2. Moving Up Lifestage

You have commitments to sustain. You may have a partner or children who need your provision. You’re beginning to think about sustaining their schooling, their future and their dreams. You also have parents who may be depending some support from you.

- Concerns are protection for yourself, own family (spouse and kids), and parents

- High-emergency fund

- You save to achieve family goals

3. Preparing Ahead

Your concern is nurturing your health and wealth. Getting prepared for the golden years is what you’re beginning to think of.

- Concerns include your retirement plan

- Protection for yourself and/or your ageing parents

- Boosting your emergency funds

- Target achieving your personal goals

- Leaving a Legacy. You want to ensure lasting golden years.

- Wealth preservation

- Plan for legacy/estate

- Protection for yourself and spouse

4. Leaving a Legacy

You want to ensure lasting golden years.

- Wealth preservation

- Plan for legacy/estate

- Protection for yourself and spouse

II. What is/are Your Objective(s) in Purchasing the Product?

- INCOME PROTECTION – Money to protect against financial setbacks (e.g. death, accident, disability)

- HEALTH PROTECTION – Money to cover medical expenses (e.g. upon diagnosis of critical illness, hospitalization, etc.)

- EDUCATION – Growing money for your child’s college education

- RETIREMENT – Money for a comfortable retirement

- LIFE MILESTONES – Money for your life milestones and other needs (e.g. Travel, Car, House)

- ESTATE TRANSFER – Money to efficiently transfer wealth to loved ones

III. What type of product(s) are you looking for to meet your objective(s) above?

- INSURANCE – Insurance product without any savings or investment component (e.g. term insurance)

- INSURANCE WITH SAVINGS – Insurance product with savings but without investment element (e.g. traditional participating policy)

- INSURANCE WITH INVESTMENT – Insurance product with investment risks borne by you (e.g. variable unit-linked)

- INVESTMENT – Investment product with no insurance protection. Risks borne by you. (e.g. mutual funds)

IV. For how long are you able and willing to contribute and keep THIS application?

- One Year

- 5 Years

- 10 Years

- Over 10 Years

- Whole Life

V. Approximate Investible Assets Per Month

VI. How do you describe your investment experiences?

- No experience

- Limited

- Moderate

- Good

- Expert

VII. How many years have you been investing in stocks, bond, mutual funds and stock market?

- No experience

- Less than 1 year

- 1 to 5 years

- 6 to 10 years

- Over 10 years

VIII. How would you describe your investment goals and the level of risk you can take?

- CAPITAL PRESERVATION: I want my capital secured even if investments provide low returns

- REGULAR INCOME: I prefer investments that provide a predictable flow of income, as opposed to funds that widely fluctuate.

- INCOME AND GROWTH: I want a regular flow of income but will accept some volatility for capital growth. I prefer investments that provide both opportunities to earn income and to grow over time, even there is a risk involved.

- CAPITAL GROWTH: I seek long term growth with some income. I am comfortale with volatility in order to achieve capital growth.

- CAPITAL APPRECIATION: I seek capital appreciation and fully accept volatility. I prefer high-risk investments with high potential returns.

IX. How much of your investible assets are you willing to invest in higher-risk investments?

- Less than 20%

- 21% to 60%

- 61% to 80%

- Over 80%

X. How long can you keep you money invested to achieve your financial goals?

- One to five years

- 6 to 10 years

- Over ten years

XI. Which statement best describes your financial situation?

Please consider your regular expenses, payment of outstanding loans, and your savings for emergencies and retirement. Which of the following statements best describe your situation?

- I cannot afford to lose much of this fund because I get my expenses for living from this.

- I do not need this fund to supplement my current income. However, this could change.

- My financial situation is stable, and I have sufficient cashflow to meet most of my requirements.

- My financial situation is secure. I can meet my emergency requirements.

If you wanted to get a quotation from Sun Life, I have a form below called Client Suitability Assessment Form.

How Long Do I Contribute to a VUL?

There are VUL’s that are designed for one-time pay, 5 years pay, 10 years pay, flexi pay and lifetime pay.

The length of your contribution depends on the product that you chose. Since VUL has investment component, you are free to top-up additional funds to increase your investment exposure.

There will be times that you may not be able to pay your premiums. It’s okay. As long as your fund value can pay your premiums, your policy stays in force. But of course, once you miss payment, you lower your chances of growing your future funds.

You choose to pay regularly like annually, semi-annual, quarterly or monthly.

Top Recommended VUL Combination

For me, the best insurance any one should have is a combination of VUL and Sun Fit and Well Advantage. For me this is the best set of life insurance, health insurance and investment program any Filipino should have because it protects you comprehensively.

- VUL should have add-ons or riders namely TDB (Total Disability Benefit), ADDD (Accidental Death, Dismemberment and Disability), Daily Hospital Income Benefit. The investment component also aims to grow your money through time.

- The Hospital Income Benefit (HIB) ensures that when you are hospitalized either by sickness or by accident, you will have reimbursement.

- Sun Fit and Well then covers 114 critical illnesses. The Sun Fit Advantage includes other benefits as well. See this sample proposal for VUL-Trad Combination