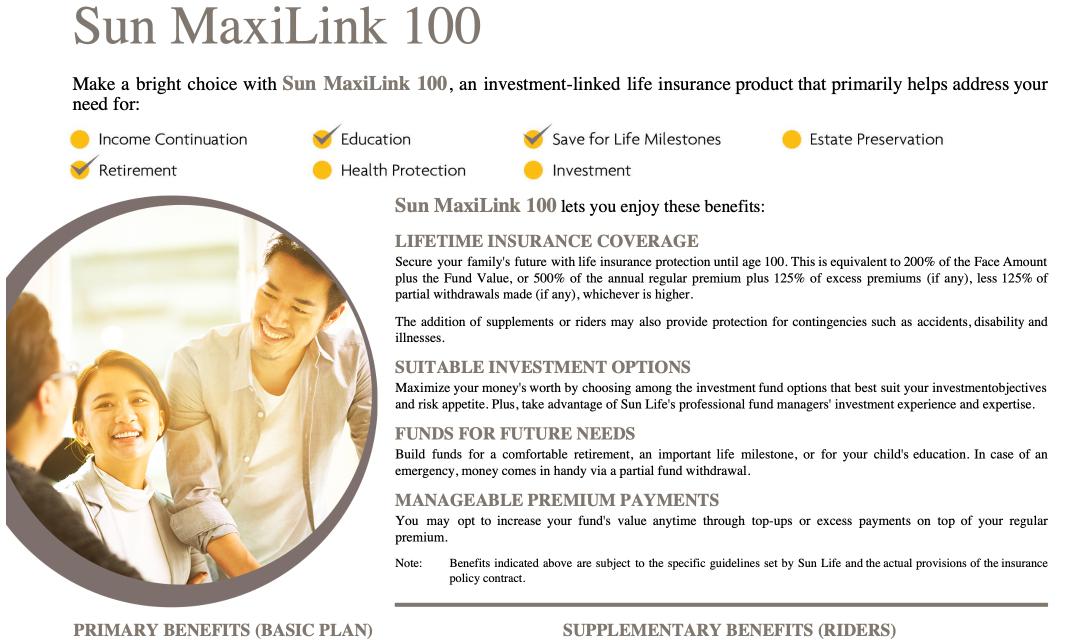

Sun MaxiLink is the latest VUL or investment-linked insurance plan of Sun Life. Its distinct feature is that it can cover you until age 100. (Maxilink Prime and Flexi are until age 88 only)

Main Benefits: The minimum death benefit you can get here is P700,000 (natural death) taken from the 200% of the Face Amount*. Your fund value will be added on top of the death benefit. These are from the premiums you pay and they are the funds where charges are also taken.

Maxilink 100 is recommended if: Your goal is to guarantee a certain amount for your dependents in case uncertain death comes while at the same time, growing a portion of your money for future needs in case that untimely death does not come.

*or 500% of the regular premium plus 125% of the excess premium, less 125% of each partial withdrawal.

Where to place your fund value

The fund value is the fund you can use in the future such as for retirement, child’s education, emergencies, or you can just leave alone for your children.

Your fund value will be placed depending on your needs and objectives. They can be:

- Bond (for emphasis on capital preservation)

- Equity (more emphasis on aggressive growth)

- Balanced

- My Future Funds – these include a specific year in the end because these funds are designed to be aggressive initially and conversation towards the end. I recommend this option for those who want to use VUL as their vehicle for a child’s education or retirement.

- Index Funds (the top-performing companies in the Philippine stock market)

Pros

The funds are handled by professional fund managers and guided by well-structured investment objectives. You won't spend time studying the stock market and fund information because the pros do them for you. Just focus on what you are best at.

Cons

Professional management does not guarantee investment returns nor protection against capital loss. This is because investments are subject to market risks, regulatory, currency, and default risks which no one certainly knows. But as an advisor, I always tell my clients that "time in the market is better than timing the market." It means that the best strategy is long-term strategy, especially when you choose index or equity funds. These are the funds which have stable growth over a long period of time such as 5 to 10 years.

What supplementary benefits can you attach?

You can also add riders or supplementary benefits to increase the likelihood of enjoying your living benefits. Common riders I recommend are:

- Total Disability Benefit

- Accidental Death

- Accidental Death, Disability, and Dismemberment Benefit

- Critical Illness Benefit

- Hospital Income Benefit

What are the fees and charges to this product?

During the tenure of Maxilink 100, it is subject to Fund Management Charge, Monthly Periodic Charge, and Cost of Insurance Charge. When partial or full withdrawal of fund value is made, it may be subject to Surrender Charge.

How will your investment fund value be assessed?

The investment value is the amount of your funds which is computed by the number of your units x the rate or NAVPU (Net Asset Value Per Unit).

It is valued every working day, and when you have a financial transaction for any day (e.g. withdrawal), the next day’s unit price (NAVPU) will be used as the reference. The rates are available via the Sun Life website and newspapers.

Can the fund value be withdrawn in case of emergencies?

Yes, you can make partial withdrawals from your Fund Value when you have emergencies. Please note that the amount to be withdrawn may be subject to applicable charges (e.g. withdrawal charges) depending on the policy year (usually higher during the early years of the policy).

However, when you withdraw funds from your fund value, it diminishes your death benefit and may result to possible termination of your policy, in case the remaining Fund Value is no longer sufficient to cover the policy charges.

When you withdraw your Fund Value in full, your policy will be deemed surrendered and terminated. Note that surrendering your policy may be more disadvantageous rather than beneficial because of the following reasons:

- you will incur surrender charges

- you lose potential investment earnings

- you lose the benefits of insurance protection

When you decide to apply again in the future, the decision will be based on your attained age (which has a more expensive premium) and your health condition at that time (which by then, you may be subject to certain health conditions).

Because of a “more riskier” health status, you may be asked for more medical exams and be possibly excluded from other coverage benefits.

It is encouraged that you maintain your policy to maximize your benefits. Moreover, if you keep your policy in-force, you may get Loyalty Bonuses (at 10th year, and 5 years thereafter).